The Billion-Dollar Aftermarket That Isn’t Supposed to Exist Somewhere between a Taylor Swift concert—the kind that…

Every entrepreneur who has built something valuable eventually asks a fundamental question: how do I protect…

Contemporary wealth preservation increasingly demands jurisdictional diversification as a response to risks that transcend conventional investment…

The Constitution of the Republic of Poland guarantees that forfeiture of property may occur only on…

Prejudgment security over taxpayer assets presents an instrument of dual character: on one hand, it safeguards…

When May Tax Authorities Encumber a Taxpayer’s Property? Prejudgment security over business assets represents one of…

How to Shield Your Business Within the Law Every entrepreneur bears the risk of poor decisions,…

When the Tax Authority Comes Knocking Asset seizure by the tax office represents the ultimate coercive…

Evidence in tax proceedings encompasses the totality of evidentiary instruments employed to establish the factual predicate…

The principle of free evaluation of evidence constitutes the cornerstone of fact-finding in tax proceedings, establishing…

The principles governing the gathering of evidentiary material constitute the foundation of fair and lawful tax…

Extraordinary Remedies Under Polish Tax Procedure The revocation or modification of a final tax decision constitutes…

Doctrinal Foundations, Comparative Frameworks, and Procedural Mechanisms The annulment of a tax decision (Aufhebung des Steuerbescheids…

This article examines the increasingly prevalent practice of utilizing Article 176 of the Polish Commercial Companies…

Requiring Transaction-Specific Evidence in VAT Fraud Proceedings Tax authorities accused a commercial enterprise of engaging in…

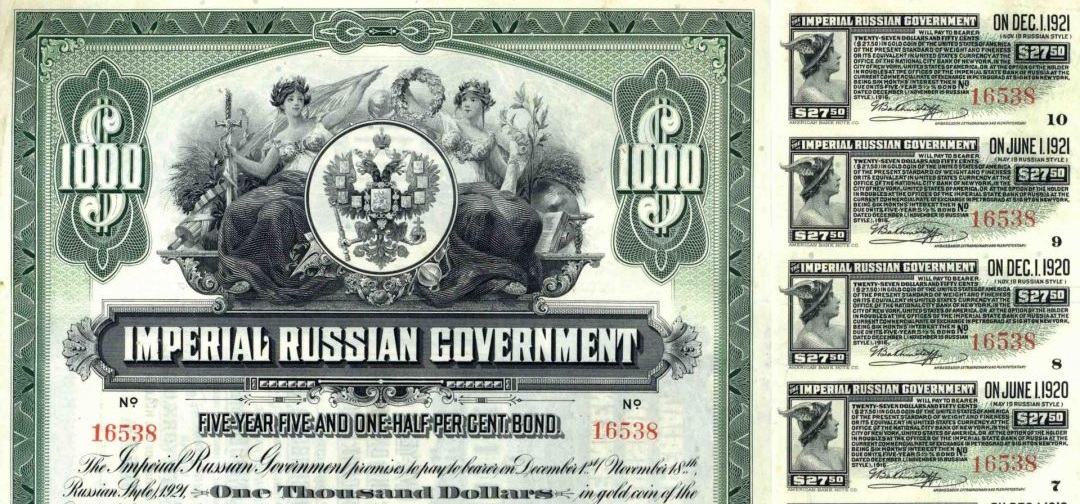

Tsarist Bonds, $225 Billion, and the New Lawfare Against Russia Twenty-five million dollars. This was the…

Official Documents, Counter-Evidence, and the Limits of Administrative Discretion This Article examines a landmark decision by…

Abstract: This article examines the intersection of taxpayer good faith and the fundamental right to deduct…

The statement of reasons accompanying a tax decision constitutes far more than a mere formality—it represents…

The Jurisprudence of Reasoned Decision-Making A certain tax dispute concerning undisclosed sources of income persisted for…

Causation, Contribution, and the Limits of Fiscal Immunity Abstract: This article examines a consequential ruling by…

Crowdfunding Services and the Limits of Taxable Supply Abstract: This article examines a significant ruling by…

When Previously Known Circumstances Cannot Justify Resumption of a Final Determination The reopening of tax proceedings…

Provincial Administrative Court in Łódź, Judgment of February 28, 2023 (I SA/Łd 745/22) Tax authorities in…

The Full 19% Statutory Rate Prevails Over Treaty Limitations Polish taxpayers may reduce their withholding tax…

Navigating the VAT-PCC Boundary Under Polish Law Abstract: This article examines the seminal 2018 decision of…

In December 2017, Poland’s Supreme Administrative Court delivered a verdict that cut through tax-authority overreach with…

Pursuant to Article 70 § 1 of the Polish Tax Ordinance, tax obligations become time-barred upon…

Published: January 12, 2022 | Updated: January 2026 The legislative amendments to the taxation of wind…

Restaurant Services vs. Food Delivery: The EU Court Ruling That Defines VAT for Fast Food When…